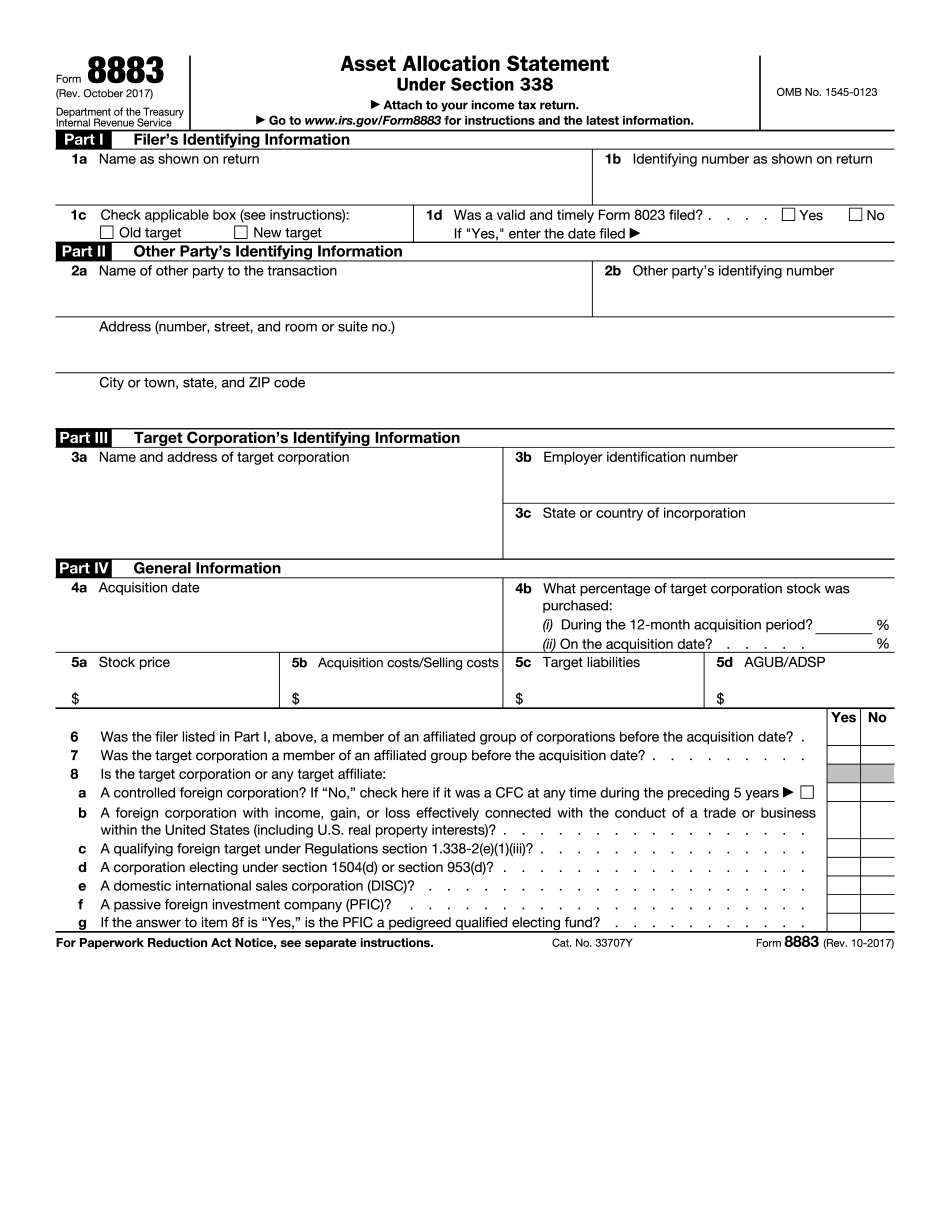

Award-winning PDF software

Form 8883 for New Jersey: What You Should Know

Section 338A does not apply to transactions that occur after January 21, 2002, that have been completed in New Jersey, but since have taken place in a foreign state or another state which does not tax companies that acquire such properties. The IRS released an update to the guidance relating to the tax application of Section 338(a) for the deemed sale of assets of a foreign corporation, which provides the following: (i) The determination of whether the entity has a permanent establishment in New Jersey shall be based solely on the facts and circumstances of each case, which may be substantially different from and in a different field of economic activity from the facts and circumstances of other cases or circumstances. Accordingly, the determination of whether a transfer or sale of property from the New T,’s New T,” corporation to other foreign corporations is a transaction that occurs in a market that is substantially different from the market in the other states included in the guidance, must be made on the basis of the facts and circumstances of each separate case, which may be substantially different from and in a different field of economic activity from the facts and circumstances of other cases and circumstances. In the case of a deemed sale transaction, if the transferor corporation will be liable to New Jersey sales taxes on the sale of property acquired by its foreign arm after such transferor is liable to New Jersey taxes on the acquisition of the property, which are equal to the highest of 5.25 percent or its highest state tax rate, at the time of the acquisition, and after any necessary local adjustments to the foreign subsidiary corporation's rate of sales tax. (Note that New Jersey rates are generally lower than the combined federal rates for New Jersey and New York). The following tables illustrate the application of New York tax laws to the transferor's corporation and the subsidiary's New T,” corporation: Table 1: New York State Income Tax with Deduction of Federal Tax on New York Sales, and Sale, of Property, from a Non-Resident New T,” Corp. to a Residency Taxpayer in New Jersey. Table 2: New York State Income Tax on the Sale of Property, from a Non-Resident New T,” Corp., to a Residency Taxpayer in New Jersey.

Online methods assist you to arrange your doc management and supercharge the productiveness within your workflow. Go along with the short guideline to be able to complete Form 8883 for New Jersey, keep away from glitches and furnish it inside a timely method:

How to complete a Form 8883 for New Jersey?

- On the web site along with the sort, click Commence Now and go to your editor.

- Use the clues to complete the suitable fields.

- Include your personal info and contact data.

- Make certainly that you simply enter right knowledge and numbers in ideal fields.

- Carefully verify the articles from the type in addition as grammar and spelling.

- Refer to aid portion for those who have any queries or tackle our Assistance team.

- Put an digital signature on your Form 8883 for New Jersey aided by the enable of Indicator Instrument.

- Once the form is completed, push Finished.

- Distribute the all set variety by means of e-mail or fax, print it out or help save on the product.

PDF editor allows you to make adjustments with your Form 8883 for New Jersey from any world-wide-web connected equipment, personalize it in line with your requirements, indication it electronically and distribute in several methods.