Award-winning PDF software

Form 8883 Vancouver Washington: What You Should Know

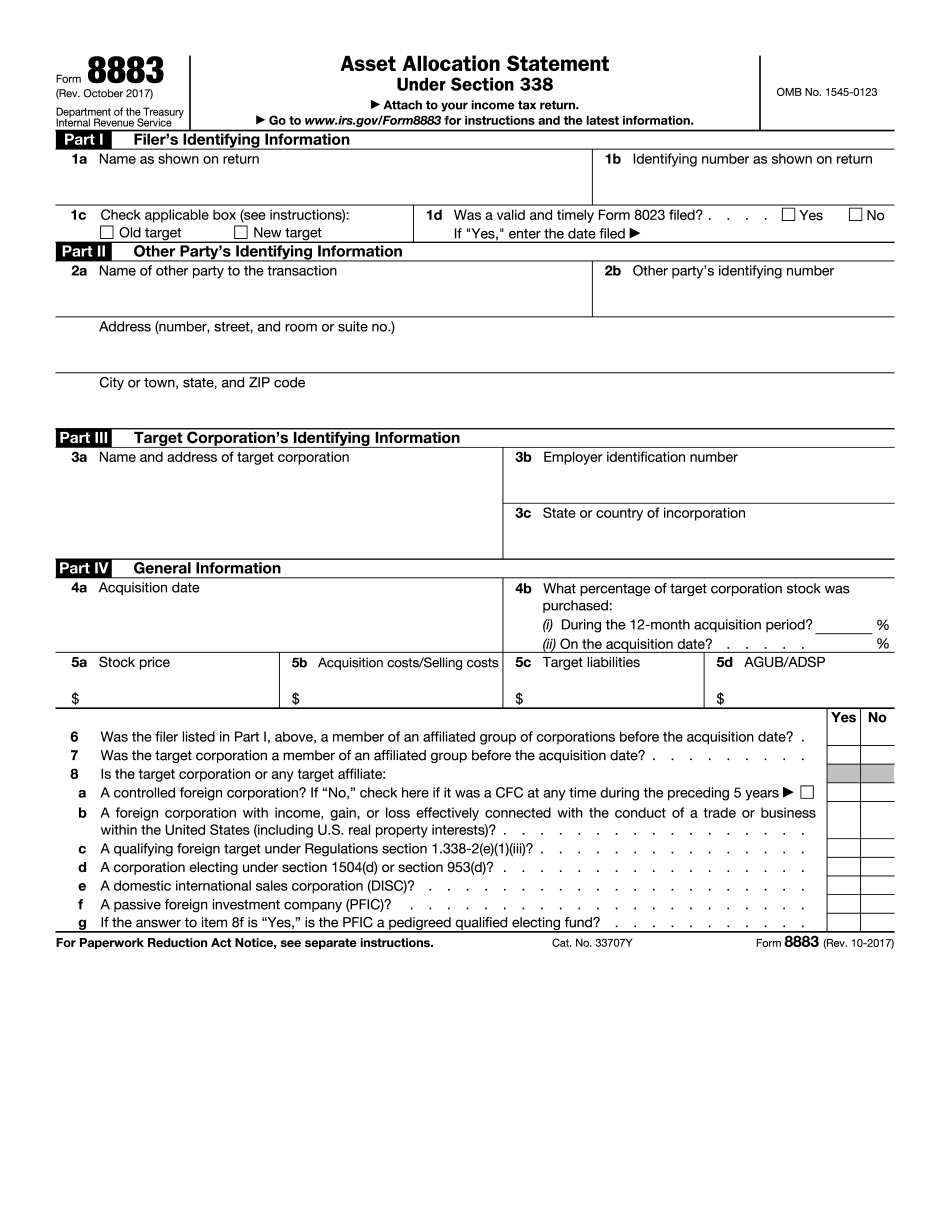

Rev. October 2017) (Tax Bulletin, December 2008). I am not sure just how the IRS intends to modify the Form 8883, to allow greater flexibility to determine the fair market value of corporate properties. (I would also recommend making another request to the Clark County Auditor to look at this.) I do have some additional insight into just how the IRS intends to modify Form 8883 for the value of corporate property. The IRS does have guidance indicating that the fair market value of property acquired from a corporation is in general the fair market value of property acquired by a corporation, and not the transfer price of the property transferred. When a corporation sells a property, there is an implicit presumption that the corporation's cost of acquiring the property is the transfer price. This assumption can be altered when the sale is for tax purposes and when a taxpayer takes into account other facts and circumstances. I believe that the value transferred is determined for use in calculating the fair market value of the property transferred, rather than an actual sale price. The IRS recognizes that under certain circumstances companies may acquire property at market value or below market value on tax- generating transactions. Generally, however, the transfer price should be used for tax purposes. While there are a number of individual cases involving IRS consideration of the transfer price in determining fair market value, the IRS does not have to approximate the fair market value of property acquired by a corporation to determine the fair market value of the property transferred to an organization under section 280E. This appears to be consistent with the way that other federal tax administration agencies have determined the fair market value of property transferred to individuals. In addition, it would appear reasonable for the IRS to treat corporate property as property that would be sold at fair market value rather than as being held for the future at less than fair market value to be determined by the company and to be paid as it is depreciated. As of the date of this blog post, the IRS has not issued a ruling on the IRS guidance. They have not made any decisions or decisions- about the fair market value of corporate properties under section 280E for the purpose of determining fair market value of the property transferred to individuals or corporations under section 280E.

Online methods assist you to arrange your doc management and supercharge the productiveness within your workflow. Go along with the short guideline to be able to complete Form 8883 Vancouver Washington, keep away from glitches and furnish it inside a timely method:

How to complete a Form 8883 Vancouver Washington?

- On the web site along with the sort, click Commence Now and go to your editor.

- Use the clues to complete the suitable fields.

- Include your personal info and contact data.

- Make certainly that you simply enter right knowledge and numbers in ideal fields.

- Carefully verify the articles from the type in addition as grammar and spelling.

- Refer to aid portion for those who have any queries or tackle our Assistance team.

- Put an digital signature on your Form 8883 Vancouver Washington aided by the enable of Indicator Instrument.

- Once the form is completed, push Finished.

- Distribute the all set variety by means of e-mail or fax, print it out or help save on the product.

PDF editor allows you to make adjustments with your Form 8883 Vancouver Washington from any world-wide-web connected equipment, personalize it in line with your requirements, indication it electronically and distribute in several methods.