Our speaker for today is Vicky Mu, an enrolled agent and certified financial planner (CFP), and the owner of American Financial and Tax. This tax preparation, planning, and representation firm was founded in Tustin, California in 1985. Vicky is known for her expertise in federal and California tax law and frequently presents at continuing education events hosted by professional organizations. She has also written numerous articles on tax law that have been published in instructional journals. In addition to her private practice, Vicky serves on two advisory boards for California state tax agencies – the California Franchise Tax Board advisory board since 2010 and the Employment Development Department's Small Business Employers Advisory Committee since 1997. She has received multiple awards for her service, legislative advocacy, and educational goals from the Enrolled Agent Association and EA and cs/ei. Vicky and her husband George reside in Boston. Thank you, Michael, for the introduction, and a warm welcome to all the attendees of today's presentation. I want to discuss a somewhat unusual and complex topic today. Please be aware that even for me, it can be challenging. The reason these elections can be complex is that they are a form of tax fiction. We report something on our tax returns as if it happened, even though it didn't. Today, we will focus on three different elections: two 338 elections (regular and H 10) and one 336 election. We will explore who can utilize these elections, how they function, and what benefits they offer to certain taxpayers. It's essential to understand the terminology associated with these elections, such as old target, new target, aggregate deemed sales price, adjusted growth DEP basis, aggregate deemed asset disposition price, and deemed liquidation. Throughout the presentation, we will clarify the meanings of these terms and which elections they...

Award-winning PDF software

Mechanics of 336 e election Form: What You Should Know

B) Availability of election. A section 336(e) election is available if seller and target enter into a written agreement. The section 336(e) election is treated as if written on the day that the S corporation target makes its first payment before any disposition, but must be filed with the seller within thirty days after making the first such payment. Definition of S corporation or S Corps. For purposes of this section, a “S corporation” is a corporation for which all the shareholders (or, for an S corp. that is a partnership, all the partners) are shareholders of another corporation, and either: (1) Each of the owners is a share owner of a partnership in which the S Corp. has a subchapter X (or CZ) tax treatment, or is an S corp. as defined by 26 U.S.C. § 1350(e). (2) (i) The S corporation is any domestic corporation with one or more Subchapter X (or CZ) tax treatment subsidiaries (including partners in such a partnership). (ii) The S Corp. has one or more qualifying S corporations or subchapter S (or CZ) tax treatment subsidiaries, or a combination of qualifying S corporations and subchapter S (or CZ) tax treatment subsidiaries, for the same taxable year; and For the purpose of this section, the qualifying S corporations are qualifying S corporations. (3) or (iii) The S corp. is a partnership, and: (A) Each partnership member and partner is a shareholder of another partnership with which the S Corp. has a tax treatment subchapter S (or CZ) tax treatment. For example, an S corporation is a qualifying S corporation if its shareholders are all partners of a partnership with which the S Corp. has a subchapter S (or CZ) tax treatment subsidiary. Similarly, the S Corp. is an S corp. with respect to a partner if there is a partnership relationship between the S Corp. shareholders (whether in the S Corp. as a general partner or as a general partner in another partnership) and either (A) A subpart F tax treatment subsidiary from which the S Corp.

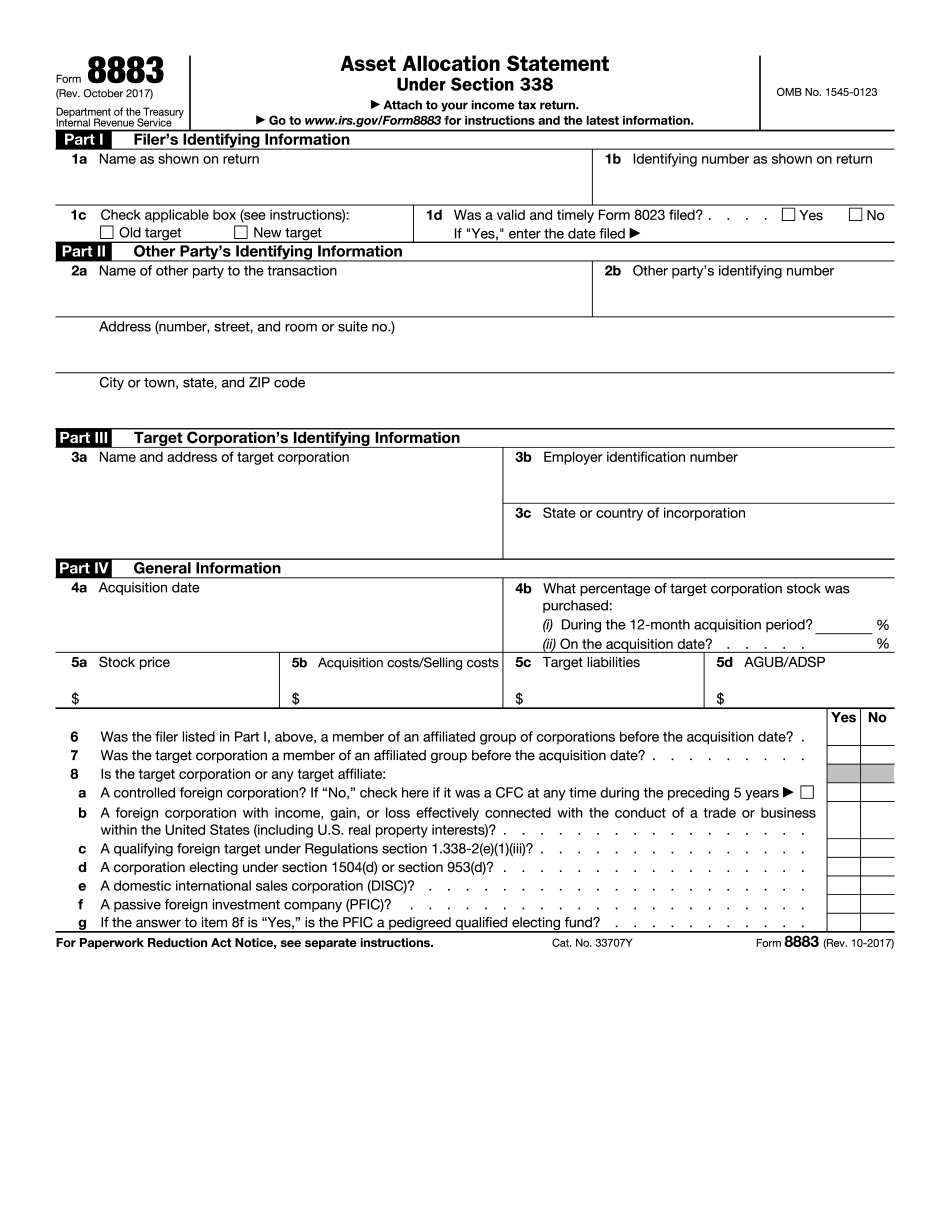

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 8883, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 8883 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 8883 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 8883 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing Mechanics of 336 e election