Hi, I'm Rich with Tax TV. I have some information for businesses interested in making a 338 election in a merger and acquisition transaction. One company purchasing another in a taxable transaction may elect to treat the purchase of stock as an asset acquisition. In a typical stock purchase transaction, the buyer does not receive a step-up in basis of the purchased assets, but rather a carryover basis. This is a problem because assets are depreciable and stock isn't. However, the tax code provides a solution. A company can make a 338 election to treat the stock purchase as a hypothetical asset purchase. This way, the buyer is given a step-up in the basis of the assets. As a result, the buyer now has a higher basis for depreciation of assets. This is especially important for intangible assets, such as goodwill. The disadvantage of the election is the recognition of gain or losses on the deemed sale as if the assets had been sold. Therefore, this only makes sense when the present value of the future tax savings from depreciation and amortization exceeds the current tax costs of the step-up. There are two types of elections, 338 G and 338 h10. The first doesn't change the tax treatment for the purchased company shareholders and is, therefore, a unilateral election made by the buyer. The second will change the tax treatment for both parties and is, therefore, a joint choice. For more information about the 338 h10 election or other M&A tax topics, search Tax TV at taxTV.com. Thank you.

Award-winning PDF software

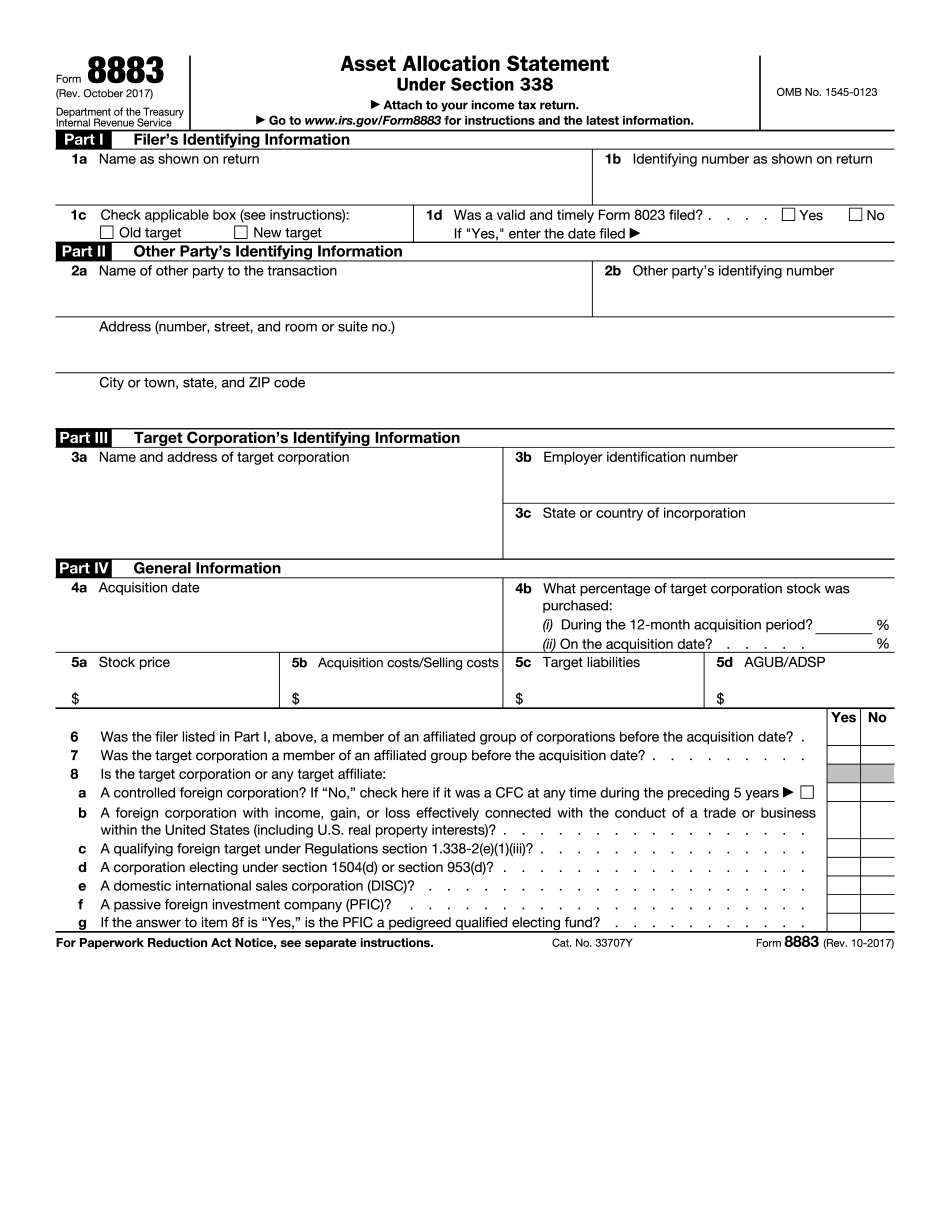

338(g) election Form: What You Should Know

S. Person who meets the following requirements may, with regard to the first taxable year after the conversion of its foreign property to United States property, take an election under section 340 with respect to each class of share of stock and each class of property held by the foreign corporation: An electing U.S. person is an individual or entity that meets all the following conditions: A. The foreign corporation has a “qualifying ownership” (defined below) of at least 10 % (or such greater percentage as may be reduced by a qualifying United States shareholder who owns 100 % of the stock or 100 % of the property) of the stock or 5% (or such greater percentage as may be reduced by a qualifying United States shareholder who owns 50% of the stock or 50% of the property) of the property held by the foreign corporation. B. The foreign corporation has a “qualifying United States shareholder” with respect to a class of share of capital stock which includes stock with at least 5% of the “qualifying ownership” of the capital stock of the foreign corporation if either of the following occurs: (1) The shareholder meets either of the following: (i) A. The number of shares of such stock is less than the total number of shares that the foreign corporation owned on the last day of the relevant taxable year of the foreign corporation, or (ii) B. The share of the aggregate fair market value of the stock that the shareholder own is the greatest of (x) 200% of the aggregate fair market value of all of such stock or (y) 5% of the aggregate fair market value of all the stock. A U.S. shareholder is an individual or entity that meets the following conditions: 1. The shareholder owns (or meets one of the following conditions: 1.1) a class of stock that includes stock with at least 5% of the “qualifying United States shareholder” share owning at least 10% of the capital stock of the foreign corporation in the relevant taxable year, and (2) the foreign corporation has a “qualifying United States shareholder” with respect to a class of share of capital stock which includes the stock with at least 5% of the “qualifying United States shareholder” share (or the aggregate fair market value of the class of stock that the shareholder owns is greater than 1% of the aggregate fair market value of all of such stock). C.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 8883, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 8883 online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 8883 by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 8883 from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing 338(g) election